International Operations

Strong foundations laid in 2015 proved a sound platform for growth in Maldives, Myanmar and Italy, expanding our footprint beyond our first overseas venture in Bangladesh. We strengthened our market leadership position in Inward Remittances as we commenced operations in Italy through our subsidiary Commex, paving the way for a new era of growth. We also expanded our horizons with the opening of a fully fledged Tier I bank in Maldives.

Bangladesh

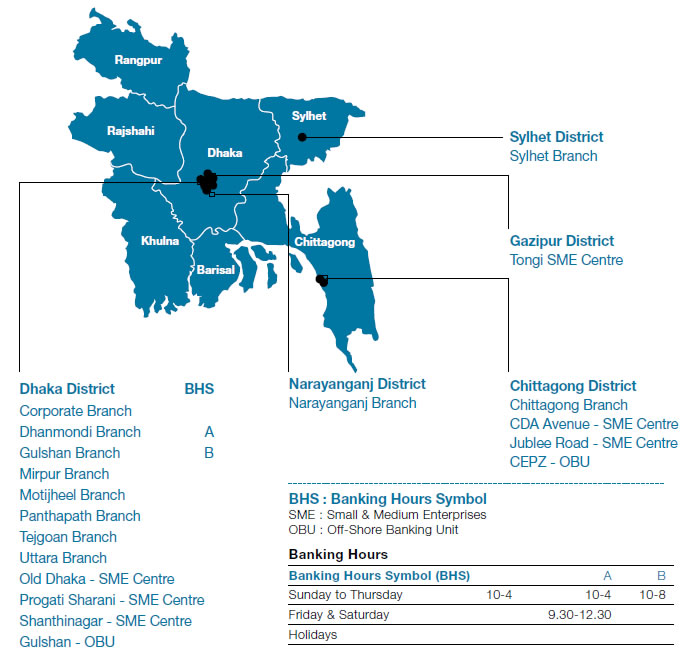

Commencing operations in 2003 with the acquisition of the Bangladesh operations of Credit Agricole Indosuez comprising five own customer touchpoints, CBC Bangladesh has grown to 39 own customer touchpoints by 2016. Rated AAA by Credit Rating Information and Services Ltd., for the seventh successive year, we are positioned for further growth in Bangladesh leveraging a wide range of products and services, technology and expertise in SME and Corporate Banking.

Economy

Bangladesh experienced a strong economic growth of 7.05% during 2016 supported by impressive private sector credit growth, foreign direct investment inflows, revived exports and increased domestic consumption. Accordingly, per capita income increased from US $ 1,314 in 2015 to US $ 1,466 in 2016 supporting improvement in social indicators. Inflation dipped from 6.1% in 2015 to 5.52% in 2016 as both food and non-food prices declined during the first half of the year although it commenced an upward trend in the fourth quarter. The Bangladeshi Taka depreciated marginally against the US $ by 0.2574% to 78.70 by the close of 2016 as the trade deficit increased by 6.13% (January to October 2016) due to growth in imports. Foreign exchange reserves stood at an all-time high of US $ 32.09 Bn, equivalent of 8 months imports. Foreign worker remittances, a key source of foreign exchange for the country declined by 11.14% during the year. Bangladesh has maintained a Ba3 stable rating by Moody’s and BB- from Standard & Poor sovereign rating with stable outlook for six consecutive years.

Banking Sector Performance

The country’s banking sector comprises 57 banks and 31 non-bank financial institutions which are regulated by Bangladesh Bank. Year on year growth in deposits and advances in November 20161 amounted to 12.78% and 13.18% respectively. A low interest rate scenario prevailed during the year resulting in interest spreads narrowing from 4.84% in January 2016 to 4.65% in November 2016. The sector was further challenged by excess liquidity with consequent impact on earnings.

Performance

CBC Bangladesh Head Office was moved to a new premises in Gulshan 2 in November 2016 and the former Head Office was converted to a Corporate Branch enhancing the proximity to its corporate clientele and visibility in the market. We also launched the latest corporate online solution enabling customers to set-up rule based payments with latest digital security features offering corporate customers the ability to streamline their payment processes. Savings customers now have access to their accounts with the launch of the epassbook which has proved popular in Sri Lanka. Performance during the year was mixed as Bangladesh operations exceeded growth targets nevertheless falling short of profit targets due to unfavourable market movements.

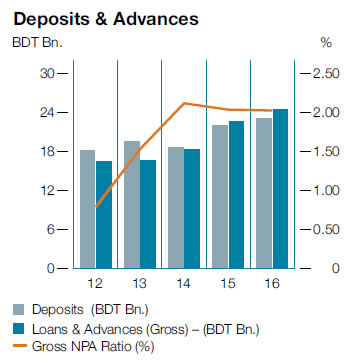

The number of accounts grew by 10% during the year, setting a platform for future growth. Deposit and advances grew by 5% and 8% respectively on a year on year basis although average growth was more encouraging at 12% and 11% respectively.(Graph 54)

Graph 54

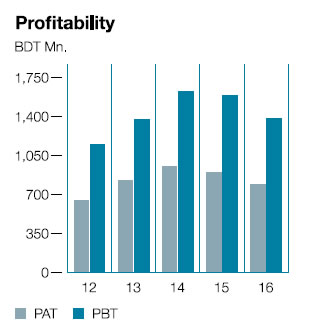

Earnings were impacted by reducing interest spreads with the Net Interest Margin declining from 6.44% to 5.11%. This was exacerbated by the lack of capital gains due to restrictions imposed by Government on long and medium-term bonds, lack of fluctuations in interest rates, increase of general provisioning due to growth in both funded and non-funded advances towards end of the year, and drop in commission and exchange income due to reduction in exports. Deteriorating credit quality remains a concern which is managed by increasing the rigour and probity of approval and monitoring processes. Inevitably, both cost to income ratio and return on assets declined to 32.76% and 3.74% in line with earnings.

Graph 55

CBC Bangladesh is launching several initiatives to improve performance in 2017, pursuing a strategy of growth with increased focus on SME, fee-based revenue sources and asset quality. Planned activities to support strategy include expanding the product portfolio, targeted marketing, streamlining processes and retaining experienced and motivated employees. We continue to align strategy to opportunities in the market whilst clearing monitoring developments in Bangladesh and with a view to realising our strategic goals.

Remittances

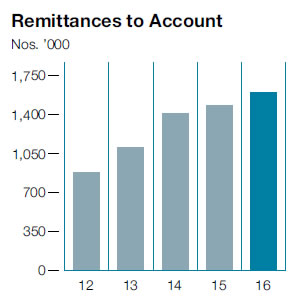

Inward remittances from migrant workers is a key source of foreign exchange for the country which amounted to US $ 6,557 Mn. by end November 2016, an increase of 3.07% over the corresponding period in 2015. The moderation in growth from 2015 attributed to declining oil prices which impacted key migrant worker markets in the Middle East and the decline in migration in skilled, semi-skilled and unskilled categories by 10.5%. Policy measures implemented to discourage unskilled female workers has also contributed to the decline in the number of migrant workers. Migration in the professional category increased by 7.6% during the first half of the year.

The Bank strengthened its position as a key player in remittances in an increasingly competitive environment by structuring products that address the concerns of both the workers and the beneficiaries. Launch of the Visa branded remittance card for beneficiaries in 2016 enables them to access a wide range of benefits which were previously available only to credit card holders, improving the lifestyle of an underbanked segment. Additional value added features include withdrawals through own or other ATMs and over the counter loans of up to Rs. 50,000. Market acceptance for the product has been encouraging with over 15,000 cards issued during the first six months from launch. As the first bank to launch a web based solution enabling access to funds in real time, we have been able to increase our market share in remittances, leveraging our branch network and technology.

Graph 56

We continued to expand our remittance channels focusing on customer convenience. Moving away from brick and mortar channels, we expanded with our partner in the Sultanate of Oman to facilitate mobile to account remittances in real time while in the Kingdom of Saudi Arabia we worked with our partner National Commercial Bank to facilitate real time transfers through the ATM network and online banking channels. In Europe, we commenced operations of Commex Sri Lanka S.R.L., our fully-owned Subsidiary in Italy, to facilitate remittances from the Sri Lankan expatriates to their families, further enumerated below under Offshore Banking.

Offshore Banking

2016 was a year to build on the regulatory approvals obtained during 2015 in Italy and Maldives and to grow in Myanmar where we have a representative office since June 2015, thus becoming first Sri Lankan bank to be granted a licence by the Central Bank of Myanmar. We have operated an advisory services model to Sri Lankan and Bangladeshi businesses looking to invest or trade in Myanmar. Aspiring to be a catalyst in increase bilateral trade between Myanmar, Sri Lanka and Bangladesh, we have received encouraging responses during the year. Although there is significant potential to play a wider role which would require a more comprehensive license.

We have discussed about the operational details of Maldivian and Italian operation under the section of ‘Subsidiaries and Associates’ on pages 102 and 103.