Natural capital

Our impact on the environment is multi-faceted, extending beyond our organisational boundaries to our clients. Firmly committed to responsible banking, we embrace a role wider than mere greening of our operations, extending our influence and resources to our clients, regardless of size. The Bank’s SEMS policy is a key pillar of our environment management framework and facilitates discharge of our environmental responsibilities.

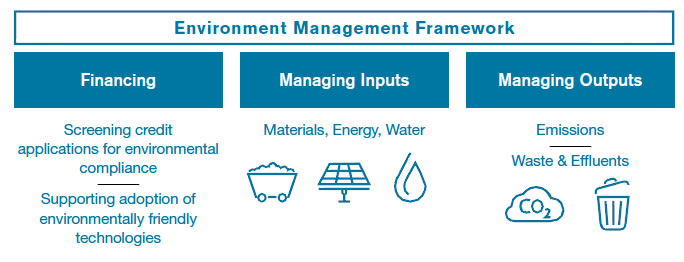

The Bank’s environment management framework clarifies our role and boundaries in managing our impact on the environment.

Figure 19

Environmentally Responsible Financing

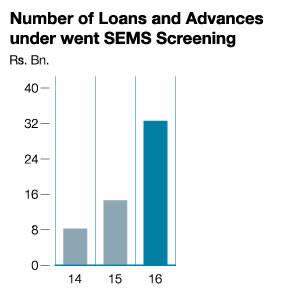

Lending responsibly is perhaps the Bank’s most significant contribution to sustainability which is done through a structured process with dedicated resources for the purpose. All loans are screened using the Social and Environmental Management System (SEMS) policy to ensure compliance with environment regulations and we engage with customers to resolve any issues identified through this process (Graph 41). The monitoring extends from the approval through implementation to ongoing monitoring. Suppliers are also screened using the same policy framework to ensure environmental compliance.

The Bank also actively supports and encourages customers to adopt technologies that support minimising their footprint through loan schemes specifically designed for the purpose with attractive rates, making a positive change.

Graph 41

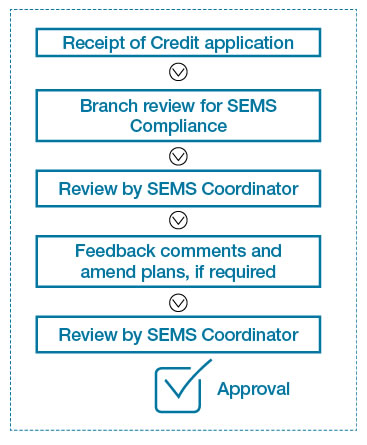

Screening of Projects for Environmental Compliance

Policies and procedures are in place under the Social and Environmental Management System (SEMS) to ensure all lending decision are made giving due consideration to environmental impacts and as well as applicable national laws and regulations on environmental and social issues. Credit Officers are trained on evaluating clients on compliance with the SEMS policy and influence customer behaviours by upholding the policy to encourage compliance. Consequently, financing is only extended to projects that are designed, built, operated and maintained in a manner consistent with the Bank’s SEMS policy.

SEMS Co-ordinator who reports to the Chief Risk Officer, validates SEMS compliance on credit proposals above a predetermined threshold.

Figure 20

In addition, periodical visits of the Bank lending officers to the financed sites ensure compliance with the environment regulations. The SEMS co-ordinator who receives upto date skills intern ensures that the lending officers are kept abreast with the SEMS policy of the Bank.

Supporting Adoption of Environmentally Friendly Technology

The Bank supports investments in renewable energy and adoption of eco-friendly technologies through Green Development Loans at concessionary interest rate for Small and Medium Enterprises (SMEs) and corporates. These loans support for investment in energy saving, energy efficiency or off-grid renewable energy projects, including investments in solar power, waste management systems, air pollution control systems, recycling or sound pollution control systems.

Managing Our Inputs

We recognise the need to manage our inputs for the betterment of the environment and our organisation. Stringent procedures are in place to manage consumption and eliminate waste.

- Managing inputs is key to managing

our cost income ratio with identified goals for materials and energy which are significant. - Water is less significant for our operations but awareness created over the years ensures inclusion of the same in to our processes.

- Bank’s Procurement Department plays a fundamental role in the day-to-day procurement of goods and services

by way of third party suppliers.

The Bank’s Supplier Code of Conduct is applicable to all suppliers supporting ethical business ranging from the environmentally accredited materials that the suppliers use to transparent, fair and honest dealings in finances and employees in their respective companies, ensuring that environmental and social standards are adhered to, across their value chain.

Materials

Material consumption comprises mainly paper and toner for printers. We continue our efforts to reduce consumption and wastage and the following initiatives contributed towards achieving this:

- Engaging with customers through our branch network and create awareness about the support provided for greening of operations. The response has been encouraging and we continue to promote Green Banking to reduce our environmental footprint.

- Launch of the e-passbook to migrate savings customers to paperless mediums while facilitating convenience. Given that savings accounts constitute 86% of total accounts, e-passbook has the potential to save a significant amount of our stationery consumption.

- During the year we have invested

Rs. 36.717 Mn. on 30 ATM machines and Rs. 52.108 Mn. on 22 units of a new generation automated cash deposit machines (CDM) that minimise the use of paper under the green banking programme. Dispensing with deposit slips and envelopes, the new machine has a stacker that can accept and count up to 200 notes at a go, enabling customers to make deposits of up to Rs. 200,000 per deposit at a time into savings or current accounts, 24 hours of the day. The same machine can also be used to pay dues on Commercial Bank Credit Cards.

Ongoing initiatives for migrating customers to paperless banking include:

- Staff-assisted customer migration to automated machines.

- The Banks’ ATM system being programmed to asked whether or not a paper transaction receipt is required from the customer.

- Directing customers to more

towards on-line banking and

mobile banking platforms. - Directing customers to choose e-statements over paper

based statements.

Programmes to reduce the amount of paper used in bank operations are in place to reduce consumption and recycle paper and choosing post-consumer recycled paper more often.

Energy

We continued the programme commenced in 2015 to convert branches to solar power, adding four more branches to the four that were operational at the beginning of the year. These branches generate 190 kWh of power which is utilised mainly to provide lighting and charge the uninterrupted power supply units of the branch. The designs of our branches also use more natural lighting and are equipped with energy efficient lighting and equipment. Branch interior and exterior signage use phot-cell technology as well. These initiatives inspire our customers to invest in renewable energy in addition to minimising our carbon footprint.

Our ATMs and IT equipment are energy efficient and only procure equipment with ‘Energy Star 5’ ratings which are compliant with the RoHS standards. We also give preference to ATM machines that function without air conditioning. As mentioned above, we are increasingly looking beyond energy requirements to ensure that equipment procured will also eliminate use of paper increasing the rigour of our procurement standards for equipment.

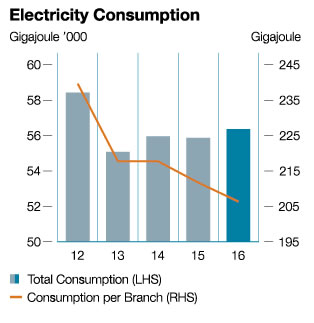

Expansion in customer touch points, increased reliance on digital platforms and growth in transaction volumes have contributed to a marginal increase in our electricity consumption by 482 gigajoules year-on-year. However, the positive impact of our efforts towards reduction of energy consumption is evinced as the energy consumption per branch has reduced to 206 gigajoules in 2016, from 212 gigajoules in 2015.

Graph 42

Water

Banks’ water consumption is mainly limited to drinking water and water used for sanitary purposes. Our employees are continuously encouraged to preserve these natural resources. On-going awareness programmes and notices are displayed for this purpose.

Managing Our Outputs

Eliminating waste in processes is a key strategic initiative supporting our long-term sustainability and social responsibility. As we have minimal effluents our policies and efforts are centred on controlling inputs and the management of emissions and waste.

Emissions

- Direct emissions (Scope 1) generated

by the Bank are negligible and comprising mainly of emissions from motor vehicles owned by the Bank used by a few senior executives. - Scope 2 emissions comprise emissions generated from purchased electricity for which the inputs are reported above together with the initiatives taken to reduce the consumption.

- Scope 3 emissions are not reported as it is not material to our operations.

Effluents and Waste

Areas of concern in managing outputs are disposal of e-waste and paper. and are managed through agreements with waste management companies who follow internationally recognised disposal practices which are monitored by the Logistics/Procurement and Information Technology Departments. During the year Bank managed to offset 163,708 kg of CO2 emission by recycling 3,843 units of e-waste and 89,124 kg of CO2 emission by recycling 111,405 kg of used paper.

Awareness programmes ensure that employees are environmentally responsible and uphold these principles in their engagements with suppliers and customers.

There is a good reason

why ‘heart’ is often

associated with ‘warmth’.

The mind, tempered with a good dose of heart will ensure that tomorrow is infused with ethics

and empathy built on a solid moral base. In the bank of the future, the guiding effect of the

heart will be required more than ever, as we deal with the growing risk associated with the

temptation thrown up by the ‘possibilities’ of an ‘unfettered’ tomorrow.

As reason is to strategy,

the heart is to ethics